{kind=link}

Saudi Arabia has received a strong demand from investors during an auction to sell two tranches of savings sukuk, in the context of declining returns on debt instruments denominated in local currencies around the world, as central banks tend to reduce the interest rate and apply unprecedented monetary stimuli to limit the economic repercussions of the Corona virus.

Al-Eqtisadiah learned that the investors bought during the auction all the seven-year and 12-year sukuk (both of which reopened to previous issues), in a sign of the fixed-income instruments investors ’keenness to obtain a part of these highly creditworthy securities.

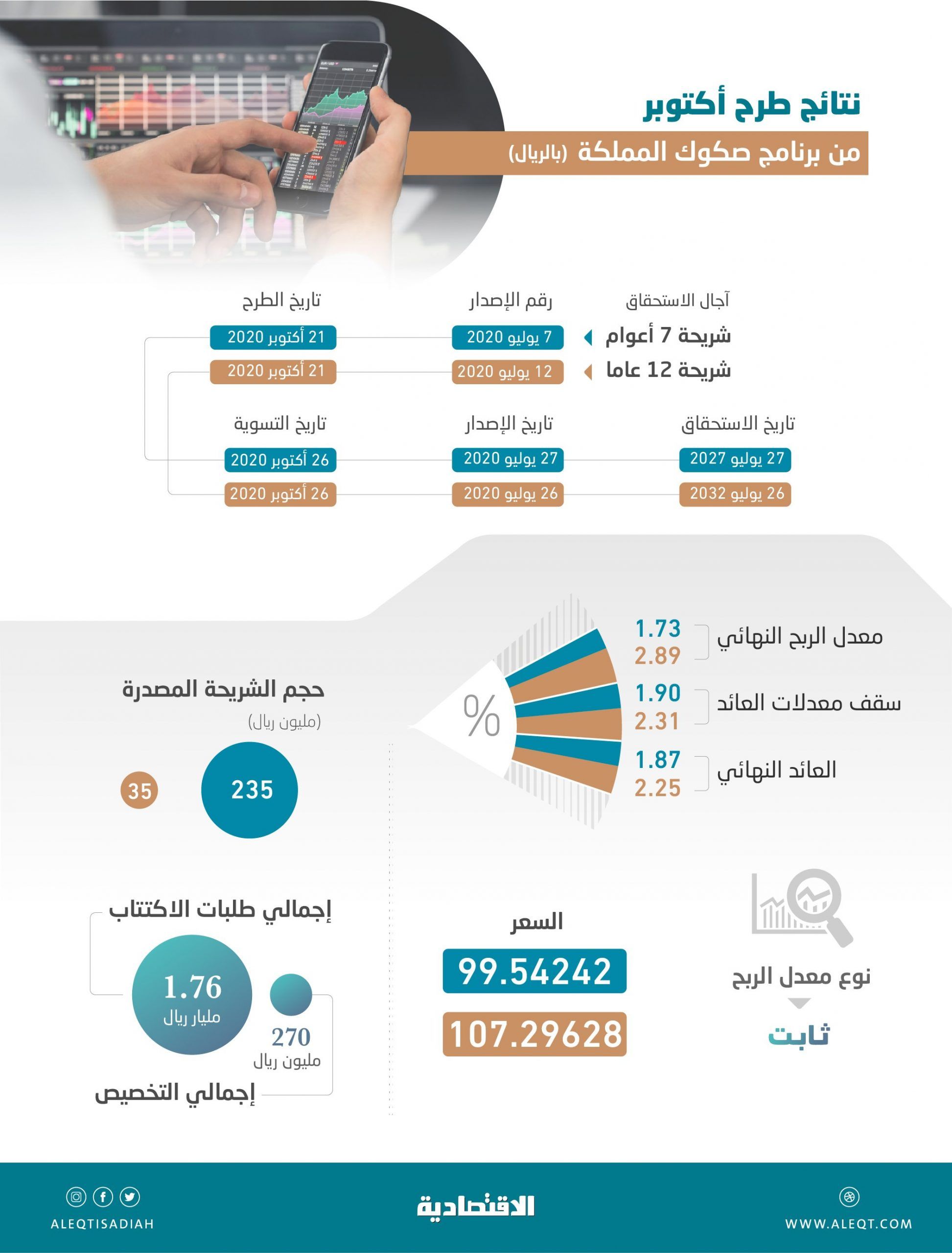

The October 2020 issuance of the Saudi government’s savings bonds received more than 1.7 billion riyals, according to an official document for the local sovereign issuance.

The document, obtained by Al-Eqtisadiah, revealed that Riyadh issued medium and long-term “dual-tranche” sukuk, the returns of which ranged between 1.87 and 2.25 percent.

According to the monitoring unit of the reports in Al-Eqtisadiah newspaper, the issue was covered more than six times for the original amount required, with the volume of requests reaching 1.760 billion riyals, compared to the actual issue size of 270 million riyals.

Investor appetite for the Saudi government issuance was reflected in the pricing aspects of the auction of savings bonds, after Riyadh paid low borrowing costs (historically) during the auction.

Al-Eqtisadiah learned that some investors had to change their policy during the submission of investment applications in fixed income instruments, as instead of subscribing to the higher ceiling of the rate of return for each segment, they placed their applications at the low levels of the ceiling of the rates of return of the two tranches, in order to ensure that they obtain The required allocation, due to the limited volume of issuance, and due to the high competition among institutional investors to obtain a portion of these securities.

A source with extensive knowledge of the issuance stated that the reason for not meeting all investor requests is due to the diversity of financing channels and options available to the sovereign issuer, as well as previous borrowing operations that took place during the first half of this year, as previously planned.

Release returns

The October issue, which will be settled, is divided into two equal tranches with a yield to maturity date for the seven-year sukuk at 1.87 percent, according to the issuance price in the secondary market at 995 riyals.

Whereas, the yield to maturity for 12-year-old sukuk reached 2.25 per cent, according to their traded price on the local stock exchange, which reached 1072 riyals during the offering.

The activity of sovereign bonds denominated in riyals is the bright spot for Saudi Arabia in the sky of global Islamic finance due to the huge size of these offerings. For example, according to a report by Standard & Poor’s, Saudi Arabia ranked second in the global sukuk industry performance by the end of 2019, when the total issuance of Saudi entities reached $ 29 billion.

Local offering

The National Debt Management Center at the Ministry of Finance announced the completion of receiving investors’ requests for its domestic issuance for the month of October 2020, under the Kingdom’s government sukuk program in Saudi riyals, where the volume of issuance was set at a total amount of 270 million riyals.

The center explained that the issuances were divided into two tranches, with the first tranche amounting to 235 million riyals, so the final size of the tranche 782 million and 800 thousand riyals for sukuk maturing in 2027, while the second tranche amounted to 35 million riyals, making the final size of the segment seven billion and 650 million riyals for sukuk maturing in 2032.

Dutch auction

Since July 2018, an auction methodology has been used that the IMF believes will give a degree of flexibility to the pricing mechanisms of new domestic issues. The July 2018 issue (seventh edition) saw the application of this methodology for the first time with debt instruments in the Kingdom, as Saudi Arabia uses the “Dutch auction”, which is the same auction that the US Treasury uses when it sells its bonds.

With the help of one of the “Bloomberg” products for auction, the primary dealers were given a specific ceiling price above which they could not price, so that the final pricing was at or below the same price ceiling.

The primary dealers were required to submit their own subscription requests, as well as those of their clients.

This auction mechanism differs from the pricing methodology, which was used in the past and revolves around determining a specific pricing range (i.e., an upper limit, an average limit and another lower bound) and asking them to price between this range, and then the final price is determined by the issuer.

Yield curve

The yield curve is defined as a line that determines the interest on debt instruments at a specific time in which the issuer has a balanced creditworthiness, but it varies in terms of maturity, as there is, for example, an interest difference between sukuk and bonds for five years and for 30 years.

And the yield curve usually takes an upward trend, which is the natural curve, but it may be reversed if the yield on shorter-term bonds is higher than the return on their longer-term counterparts, and Saudi Arabia has a natural yield curve, whether with its local or hard currency denominated issuances.

Since 2019, Saudi Arabia has succeeded in extending the maturities of sukuk in the local market through new issuances that include 12, 15 and 30 years, in order to complete the risk-free yield curve, which contributes to supporting various markets, including real estate debt markets.

The same thing was repeated in 2020 when it saw its dollar issuance of maturities of seven years and 12 years, and for the first time a bracket of 35 years, all of which came during separate maturities, contributing at the same time to prolonging the period of those benefits, in accordance with the state’s public debt management policy.

And workers in fixed income markets use the measure of “return to maturity”, in order to calculate the future return of a debt instrument if it is held until the time for it is amortized.

This measure determines the feasibility of investment or not, and this indicator is frequently used among investors to make comparisons between the annual returns of debt instruments, regardless of their maturities.

Individual participation

The issuance of this month is expected to support the stock of savings bonds available for individual investments in the secondary market. The decision to activate the reduction of the face value of the listed government sukuk to be accessible to individuals, starting from June 2019. This means that Saudi Arabia has opened the way for its citizens to participate in supporting development projects in the country, in a progressive step in line with many countries around the world. That follow this approach.

The economic reforms that pervaded fixed income markets in Saudi Arabia contributed to making the issue of individuals investing in sukuk possible after reducing the face value of the sukuk to one thousand riyals, compared to one million riyals before that.

Developing from “scratch” pays off

The credit rating agency “Moody’s” said in a report during the third quarter of 2020 that Saudi Arabia’s investment in developing the local government bond and sukuk market is paying off with doubling the financing needs, describing the Saudi sukuk market as deep and well-performing.

In a report, the agency stated that over the past three years, the Saudi government has developed from “scratch” a deeper domestic sukuk and bond market, and is increasingly functioning well, which has allowed it to benefit from the growing domestic and international demand for fixed income assets in compliance with Islamic law.

To facilitate local issuance under the program and to further improve the liquidity of the sukuk market, in July 2018 the government established a program for the primary trader of local government sukuk. Moreover, in April 2019, the government lowered the minimum subscription size to 1,000 riyals ($ 267) from one million riyals ($ 266,666) to facilitate individual participation and allow mutual funds to establish dedicated government sukuk funds.

The government has also been able to significantly extend the periods in domestic sukuk issuances to a weighted average of about 17 years in 2019 from about six years in 2018, which reduced the risks of refinancing by extending the total maturity of the government debt.

In August 2020, the Capital Markets Authority approved a decision allowing non-residents to directly invest in listed and unlisted local sukuk instruments, which – over time – will improve the liquidity of the secondary market by supporting the gradual expansion of the investor base in Saudi Arabia, especially when it becomes It is also possible to settle transactions in domestic sukuk through one of the major international central securities depositors.

Slow down debt growth

The Saudi Ministry of Finance allowed its public debt to grow during the current year 2020 from what was planned due to the Corona crisis, for the sake of financial sustainability, which preserves the gains, ensures the continuity and sustainability of economic growth and progress, and provides basic requirements for citizens.

According to its preliminary data for the 2021 budget at the end of last September, the Ministry of Finance expected an increase in public debt in 2020 to 854 billion riyals, equivalent to 34.4 percent of GDP, compared to its prediction before the pandemic at 754 billion riyals, which would then constitute 26 percent.

The total debt expected for the current year 2020 is an increase of 26 percent from what it was in 2019, which amounted to 678 billion riyals at the time, an increase of 176 billion riyals.

But the finance targets a slowdown in the growth of public debt since the beginning of next year 2021, as the debt in 2021 was estimated at 941 billion riyals (32.9 percent of GDP), with a growth of 10.2 percent over the previous year.

It also targets the volume of debt at 1.016 trillion riyals in 2022 (33.4 percent of output), with a growth of 8 percent over the previous year, then 1.029 trillion in 2023 (31.8 percent of output), and a growth of 1.3 percent from 2022.

This comes after the debt growth recorded 21.1 percent in 2019, about 26.3 percent in 2018 and 40 percent in 2017, while its growth in 2016 was about 122.5 percent.

Saudi Arabia had earlier amended the ceiling for public debt from 30 percent of GDP to 50 percent, and despite this, the Ministry of Finance expects not to reach the new ceiling in the medium term, as the ceiling was raised with the increase in the need for financing to face the repercussions Pandemic.

The Saudi finance allowed higher levels of the budget deficit in 2020 than it was planned before the Corona crisis, but the fiscal policy aims to gradually reduce the deficit levels in the medium term to support the stable financial environment and stimulate investment.

Saudi Arabia will pursue flexible policies that keep pace with local and international developments, which in turn contribute to mitigating the effects of this crisis and confronting it with a high level of efficiency.

Saudi Arabia will also continue to assess developments and take appropriate financial policies to raise financial performance and to ensure the sustainability of public finances in the medium and long term.

Expanding financing options

When a company touches the door of debt markets, this means that this company has reached an important stage of maturity and development, as it has expanded its financing options, thus bypassing the stage of its total dependence on bank loans.

Historically, there are no diversified financing channels for Saudi companies, due to their reliance on bank loans, as well as the stock market.

Economic Reports Unit

These were the details of the news Strong investor demand for two types of Saudi sukuk … and... for this day. We hope that we have succeeded by giving you the full details and information. To follow all our news, you can subscribe to the alerts system or to one of our different systems to provide you with all that is new.

It is also worth noting that the original news has been published and is available at saudi24news and the editorial team at AlKhaleej Today has confirmed it and it has been modified, and it may have been completely transferred or quoted from it and you can read and follow this news from its main source.