We show you our most important and recent visitors news details Challenges for bank and insurance green and sustainability hybrids in the following article

Hind Al Soulia - Riyadh - LONDON — Early signs of a green or sustainability-linked hybrid capital market for banks and insurers highlight the emerging importance of ESG factors for investors. It also places a spotlight on the issuers' ESG strategies. The potential influence of ESG credit factors on our ratings depends on our opinion of whether they are material and relevant to the issuer's capacity and willingness to meet its financial commitments. We welcome initiatives that improve disclosure and credibility around ESG credit factors, policies and aims, which can include issuing green or sustainability-linked instruments.

Banks and insurers are frequent issuers of hybrids given the importance of regulatory capital for these sectors. Green and sustainability hybrid market developments bring several challenges, however. An investor's view of the role of a green or sustainability-qualifying instrument may not always match the regulatory view of the role of a hybrid that is part of a prudentially regulated issuer's regulatory capital base.

Investors in green or sustainability-linked bonds typically consider the impact that the bond proceeds or incentive structures can have on ESG factors. Instruments that qualify for a green label generally involve an issuer commitment to earmark the proceeds for a project or activity that meets specific characteristics related to climate or environmental benefits.

Sustainability-linked bonds issued to date typically have features (such as a coupon) that will vary depending on whether the issuer achieves predefined sustainability or ESG objectives over a specified time line. Some investors have mandates specifying that bonds must have such green or sustainability-linked features to be included in a particular portfolio.

Banks and insurers have to date mainly issued such instruments as senior bonds. We are now seeing growing interest in using green and sustainability-linked structures to tap the hybrid capital market, in which banks and insurers are frequent issuers of deferrable subordinated instruments that qualify as regulatory capital. Green hybrids, for example, have so far only been issued by a handful of banks and insurers and we think they face several challenges in developing this asset class.

For these issuers, regulators expect regulatory capital to be available to absorb losses associated with any part of the business (as do we when including such instruments in our capital measures). This means issuers might have to stop payments on these hybrids because of problems associated with activities that contravene green or sustainability principles.

For example, a bank might have to stop coupons on a green hybrid if the bank incurred such heavy losses after lending to a polluting borrower that its regulatory capital ratios came under pressure. This could happen even if the hybrid had been issued specifically to finance green projects and if investors held the instrument in a green fund. Investors in green or sustainability-linked hybrids therefore bear broad risks in the issuing companies.

Green or green-ish?

We consider that the concept of capital fungibility creates a tension with the concept of earmarking proceeds from a hybrid to finance specific activities. Hybrid proceeds have to be available to meet losses from any part of the business or else the instrument will not be eligible for regulatory capital (or included in our own capital measures).

Unlike standard senior bonds, where the proceeds can in theory be directly applied only to a specific business use, banks and insurers also leverage up capital resources to fund their balance sheets. $1 billion of hybrid proceeds will support much more than $1 billion of activities on a bank or insurance balance sheet. This is why we believe investors in green or sustainability-linked hybrids are also indirectly financing more activities than those earmarked in a prospectus.

Bank and insurance hybrids may be green or sustainability-linked by label (and indeed by issuer intention) but end up being light for specific structural commitments. We have seen several caveats and qualifiers regarding "use of proceeds" language and we anticipate this will continue given the inability to ring-fence green capital from non-green (or sustainability-linked from non-sustainability-linked) from a regulatory capital and equity content perspective.

This is not to imply that banks and insurers are anything other than serious about their green and sustainability objectives (and we note that all investors in green and sustainability-linked bonds are ultimately exposed to the overall business risk of the issuers), but such hybrids may not match the investment mandate of some green and sustainability investment portfolios. Given the challenges regarding specific hybrid terms, we expect that banks and insurers may be better able to tap this asset class based on the green or sustainability credentials of their broader business models than on the necessarily imperfect ring-fencing of individual hybrids.

In the meantime, bank and insurers issuing green and sustainability hybrids will have to navigate the potential for differences in expectations between investors and regulators about how a hybrid might be used in a stress scenario; the potential for changes in what investors expect from a green-labeled or sustainability-linked instrument, as well as associated regulatory risk; and any resulting reputational risks or financing cost volatility. We also think that bank and insurance regulatory approaches toward green and sustainability related assets and liabilities may evolve as regulators look at ways to address climate-transition and climate-physical risks for banks, insurers, and broader financial stability more directly.

Issuance trends and investor reception

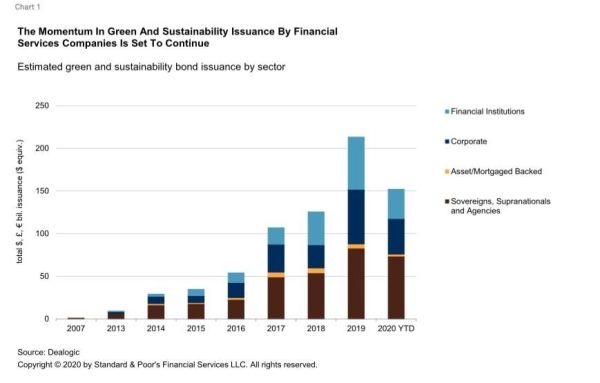

We expect growing demand for green and sustainability assets will encourage the incremental supply of such hybrids even if the limited price and diversification benefits seen by these issuers to date continues. Green and sustainability subordinated bond issuance has significantly lagged that of senior or secured asset classes (see charts), we think largely because of investor concerns that capital fungibility creates less clarity on the investor's exposure to green and sustainability-related behavior. While recent green subordinated issues by banks and insurers have not, in our view, convinced investors that they have removed exposure to non-green activities, they do show a modest degree of investor diversification and noteworthy ESG credential signaling.

We estimate that pricing benefits versus conventional issuance currently decrease from around 5-10 basis points (bps) for senior unsecured bonds to 0 bps (that is, no pricing benefit) for bank Additional Tier 1 (AT1) instruments. This dynamic, we believe, may reflect questions surrounding the structural credibility of the greenness given the fungibility of capital (Interestingly, bank issuers have been able to achieve a pricing benefit for MREL-eligible green bonds at the senior level, even though the fungibility argument does apply to these instruments as they have bail-inable loss-absorbing capacity and can be used to recapitalize the bank in the event of a resolution, although admittedly these instruments would likely absorb losses later than AT1 instruments.)

That said, the rapid development of the green and sustainability bond market, and our expectation that sustainable investment mandates will grow, suggest rising demand that in turn will encourage more issuers to introduce green or sustainability-linked hybrids to complement existing senior and secured funding programs.

The importance of green and sustainability issues means that labeling and disclosure will improve

While the taxonomy of green and sustainability-linked bonds and investor mandates is still inconsistent, we believe it is set to improve. For one, we expect the frameworks used by investors to evaluate how green or sustainable certain funding instruments are will evolve. We also anticipate issuer communication will become more sophisticated to both address investors' structural sensitivities, and to demonstrate increasing commitment to addressing climate change and upholding other related objectives.

For example, better green bond annual reporting/auditing and more explicit commitments to maintaining representative volumes of green versus conventional hybrids, to mirror risk-weighted assets, are potential outcomes as issuers look to manage increasingly relevant ESG reputational risks.

We also expect improvements in disclosure by banks and insurers due to their participation in initiatives such as that of the Taskforce for Climate-Related Financial Disclosures (TCFD) that asks that business leaders disclose to investors how climate change might affect their businesses either directly, or through their customer or supplier networks. Such disclosures are helpful in understanding the liability, climate-transition, and climate-physical risks of a specific company as well as a company's strategy to manage or mitigate those risks.

Rating and equity content considerations for green and sustainability-linked hybrids

We assess green and sustainability hybrids to determine equity content and assign issue credit ratings using our hybrid capital criteria, in the same way we assess all other hybrids. We only classify green and sustainability hybrids as having intermediate or high equity content if they comply with all the qualifying characteristics as set out in our methodology. This means the hybrid will have no equity content if it has any green or sustainability-related trigger that we consider equivalent to a step-up or any other instrument feature that contradicts the characteristics for intermediate or high equity content.

For banks and insurers, we classify the hybrid as having no equity content if a green or sustainability feature would jeopardize the regulatory treatment of such hybrid instrument. In practice, we expect that issuers will look to word these features in such a way that the regulator will include the instrument in the relevant regulatory capital category, and that this will usually mean that the hybrid can be used to absorb losses anywhere in the issuer's business. We've already seen this in several green-labeled hybrids issued by banks and insurers, such that the hybrids met all the usual regulatory requirements for the regulatory capital category.

Sustainability-linked instruments typically build in a feature that incentivizes the issuer to meet a predetermined sustainability target by a particular date, for example by penalizing the issuer if the target is not met, or potentially by lowering the cost of the hybrid if it is achieved. For such hybrids to be eligible for intermediate equity content under our criteria they must be able to conserve cash if the issuer's creditworthiness weakens, and the all-in cost must not increase if a sustainability target is missed.

If the cost of servicing a hybrid, or the likelihood of redeeming it, increases in response to deterioration of the issuer's creditworthiness, we would assess the hybrid as having no equity content. We would hold this view regardless of whether the considered step-up or one-off penalty were above or below 25 bps, if it is a one-off payment or a permanent feature, or if it is triggered before or after five years after the instrument was issued. Our analytical approach would be the same even if the stipulation that the hybrid investors would receive a higher payment if sustainability goals are not met is not in the hybrid prospectus, but instead in other related documentation.

This is because our analysis of a particular hybrid's documentation is not limited to the offering circular, prospectus, information memorandum, or agreement containing the legal terms and conditions. We also review associated documentation that is relevant to how the issuer will use the instrument, such as guarantees, deeds, waivers, covenants, and other contractual and transactional documents.

Incorporation of ESG factors into financial services ratings

ESG risks and opportunities can affect an entity's capacity to meet its financial commitments in many ways. We incorporate these factors into our ratings methodology and analytics, which enables analysts to factor in near-, medium-, and long-term impacts — both qualitative and quantitative--during multiple steps in the credit analysis. Strong ESG credentials do not necessarily indicate strong creditworthiness.

We define ESG credit factors as ESG risks (or opportunities) that are material and relevant to an obligor's capacity and willingness to meet its financial commitments. This influence could be reflected through a change in the size and relative stability of the obligor's current or projected revenue base, its operating requirements, the emerging risks it is exposed to, its earnings, cash flows or liquidity, or the size and maturity of future financial obligations. — S&P Global Ratings

These were the details of the news Challenges for bank and insurance green and sustainability hybrids for this day. We hope that we have succeeded by giving you the full details and information. To follow all our news, you can subscribe to the alerts system or to one of our different systems to provide you with all that is new.

It is also worth noting that the original news has been published and is available at Saudi Gazette and the editorial team at AlKhaleej Today has confirmed it and it has been modified, and it may have been completely transferred or quoted from it and you can read and follow this news from its main source.

{kind=link}