We show you our most important and recent visitors news details The global economy begins a slow mend as COVID-19 eases unevenly in the following article

Hind Al Soulia - Riyadh - NEW YORK — The story of the pandemic-driven steep drop in output is by now familiar. Countries imposed strict social distancing measures to slow the spread of the virus and keep cases from overwhelming health systems.

Businesses that were able to function remotely moved to working from home, while people-to-people businesses saw an unprecedented collapse of activity. GDP declined on the order of 30% to 40% at an annualized rate for a one-quarter shutdown in China (January-March), much of Europe (spanning the first and second quarters) and the US (April-June).

Services bore the brunt of the pain, in contrast to a typical business cycle downturn. Unemployment rates varied substantially across countries; they are highest in the US, although pressures to reduce employment due to plunging demand were present everywhere.

In Europe and Asia these pressures showed up mainly as reductions in hours worked combined with modest rises in unemployment rates, while in the U.S. the outcome was a meteoric rise in joblessness. The speed at which activity collapsed was unseen in modern economic history (1).

Unprecedented drops in output led to unprecedented policy responses. Central banks quickly took benchmark rates back to zero — if not there already — or to fresh all-time lows (2). They also intervened in money markets and commercial paper markets to ensure orderly trading, liquidity, and price discovery.

In addition, they stepped up quantitative easing (government bond purchases) to lower yields, ease financial conditions, and support asset prices and demand. Importantly, these operations were extended beyond public debt to high-quality corporate debt (3).

This was essentially the Global Financial Crisis playbook, enacted with more speed and agility, and the result has been a V-shaped recovery for many key financial variables.

The change in fiscal policy was more profound, although the effects will take longer to bear fruit. Governments moved with varying degrees of boldness with two objectives: containing the damage to firms and workers hit by social distancing regulations, and laying the foundations for the recovery.

These are intertwined. Direct payments to firms were aimed at providing some offset for missing revenue flows, conditioned on keeping workers on the payroll, albeit with reduced hours (4). Other measures included direct payment to households, tax breaks, and deferments.

The numbers were stunning: COVID 19-related public spending, including expenditures as well as guarantees, was 11% of GDP in the US and 25% in the eurozone (but just 3% in China) (5).

Europe's fiscal response at the regional level was particularly noteworthy as the need for a common response to the COVID-19 shock overcame longstanding objections from northern countries to more centralized spending.

Status Report: Mid-2020

The health policy response to the COVID-19 outbreak is — for the most part —working so far. Infection curves have flattened in many countries and social distancing restrictions are now being eased.

The worst of the economic and financial shocks now appear to be behind us as activity is gradually recovering. High frequency data from the past two months show that the steady rebound that began in China has moved to Europe and the US.

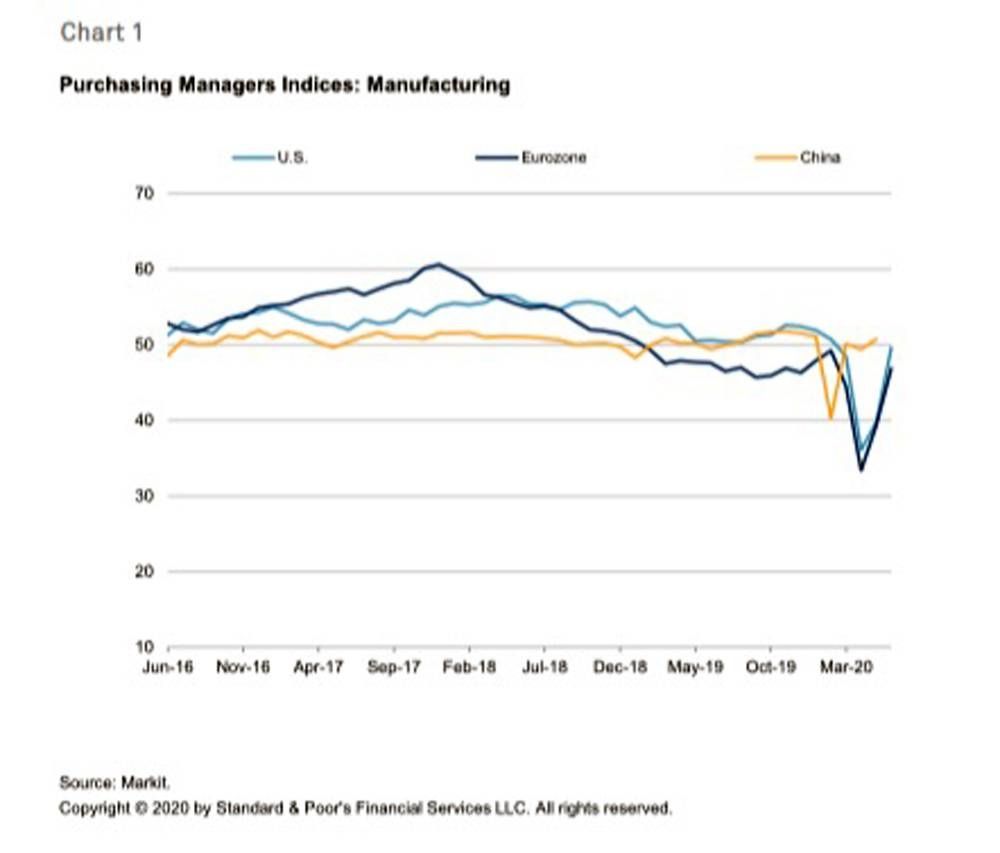

This assessment includes nonstandard data such as traffic flow and other mobility data, as well as standard indicators such as purchasing managers indices and sentiment readings.

The pattern across both types of indicators is consistent. People are moving around more frequently and spending has begun to rise, although we remain well below pre-COVID-19 activity levels (6). Retail sales numbers and, in the US, employment numbers have picked up as well.

Importantly, the service sector and small and midsize firms that were hit harder than larger ones in the downturn are now lagging in the rebound. Weak demand pressures have translated to lower and falling inflation numbers almost everywhere.

While the COVID-19 narrative across East Asia, then Europe, and the US has been broadly consistent despite variations in the intensity of measures, emerging markets are struggling to contain the spread of the virus.

Infection curves aren't flattening at the same rate as elsewhere. Indeed, the global epicenter of the virus has now shifted to Brazil. This owes to a number of factors, including enforcement, political will, the trade-offs between economic activity and health outcomes, as well as the capacity of health sectors.

This split between developed economies and emerging markets, which continues to grow, risks more permanent health and economic damage to the latter.

Our Revised Forecasts

S&P Global Ratings acknowledges a high degree of uncertainty about the evolution of the COVID-19 pandemic. The consensus among health experts is that the pandemic may now be at, or near its peak in some regions, but COVID-19 will remain a threat until a vaccine or effective drug treatment is made widely available, which may not occur until the second half of 2021.

We are using this assumption in assessing the economic and credit implications associated with the COVID-19 pandemic (see our macroeconomic and credit updates here: www.spglobal.com/ratings). As the situation evolves, we will update our assumptions and estimates accordingly.

While the recovery has begun roughly in line with our previous report, we have lowered our global 2020 GDP forecast by more than 1 full percentage point to —3.8%. This mainly reflects weaker outlooks for emerging markets, in particular India (7). The outlook for advanced economies and China remains broadly unchanged, as do our forecasts and narrative for 2021 through 2023.

In terms of COVID-19 assumptions, we adopt the consensus among health professionals: a vaccine or effective treatment will be found by mid-2021 and that it will be widely disseminated by the end of next year. (The credit angle to our macro forecasts can be found in the companion document "Global Credit Conditions: The Shape Of Recovery: Uneven, Unequal, Uncharted," published July 1, 2020.)

US

The spread of COVID-19 was slowing, but concerns remain. Infection rates have declined sharply in the states hit first and hardest but continue to rise in the south and west. All states have begun to reopen their economies, although at differing speeds, beginning with construction, manufacturing, and limited retail.

Activity indicators have bottomed, and many are now improving — including consumer and household sentiment, albeit from very low levels. In the labor market, jobs increased in May and the unemployment rate fell to 13.3% from 14.8% following a brutal surge in initial jobless claims by over 40 million since late March (8).

Government policy to contain labor market damage has been uneven due to delays, with payments not always aligned with sectoral and geographic needs. More fiscal support is likely owing to ongoing labor market and small and medium enterprises (SME) stress, as well as pressure on state budgets. However, "stimulus fatigue" as the US approaches elections may delay timing.

Financial market pressures have eased following an "alphabet soup" of interventions by the Federal Reserve; we see no substantive changes in monetary policy in the next 12 months. Consumer prices were flat year-on-year in May, with core inflation up just 1.2%.

Absent a sustained rise in inflation above its target, the Fed will not raise its policy rate until the labor market is largely healed. We expect the Fed to keep rates on hold until at least 2023 (9).

With around 25 million workers dislodged from their work in some form or another, according to Federal Reserve Chairman Jerome Powell, the economic outlook is extremely uncertain, which means the Fed could reach further into its policy toolkit later this year and beyond.

Our growth forecast is largely unchanged at-–5.0% in 2020, 5.2% in 2021, about 3.0% in 2022, and 2.8% in 2023.

(For more details on our US macroeconomic view, see "The US Faces A Longer And Slower Climb From The Bottom," published June 25, 2020.)

Europe

With the virus curve flat across much of the continent, Europe has embarked on a steady but uneven recovery. A range of indicators from traffic patterns to health stringency shows activity normalizing fastest in Germany and slowest in Spain. As elsewhere, the recovery has been more robust in manufacturing than services and for larger firms relative to smaller ones. Policy has been quite effective overall.

Financial conditions show a V-shaped recovery with liquidity and spreads normalizing accompanied by a strong increase in loans to corporations, driving a strong credit impulse. Inflation remains well below target, reflecting weak demand.

Governments have launched a series of actions to support SMEs and the labor market (over one-quarter of the eurozone labor force is on some type of short-term working scheme), as well as the hardest-hit sectors, including tourism and autos. Opening intra-EU travel, currently under discussion, will be key for southern European countries in particular given their reliance on tourism.

Our eurozone GDP forecast is lower than previously, as we have marked down our expectations for France and Spain, as well as the UK. We now see eurozone GDP contracting 7.8% this year, and recovering to 5.5% growth in 2021, 2.9% in 2022, and 2% in 2023. The recently announced EU Recovery Plan gives upside risk to our forecast (10).

(For more details on our eurozone macroeconomic view, see "Eurozone Economy: The Balancing Act To Recovery," published June 25, 2020.)

AsiaPacific

China and East Asia were first in, first out of the pandemic and serve as a leading indicator for the rest of the world. In general, inflection curves have remained flat and policy support is working. This leads us to take a relatively optimistic view of the region. Important exceptions are India and Indonesia. China continues a steady recovery, with tech and manufacturing performing better than services.

Vehicle sales have recently begun to rebound. The SME sector has been slow to respond, which has weighed on employment. In response to the slower-than-expected recovery, the authorities have been ramping up stimulus measures with the credit impulse now 5 percentage points of GDP (in the Global Financial Crisis it was 8 percentage points).

We forecast a recovery nearly back to the pre-COVID-19 output path by 2022 as the supply side of the economy remains largely intact; however, rising US-China tensions are a medium-term risk, including to productivity growth. Elsewhere, Japan is struggling to recover, weighed down by weak consumption and capital expenditure, while in Korea and Australia, the hit to growth has been less than feared.

We retain our 1.2% growth forecast for China, along with 7.4% next year and around 5% in 2022-2023. Additional fiscal stimulus could provide some upside to our below-consensus outlook. We have lowered our forecast for Japan to —4.9% in 2020.

Finally, India has been hit extremely hard by COVID-19, with the informal construction and services sectors suffering an enormous downturn. We now see GDP contracting 5.0% in fiscal-year 2021 (ending in March) from 1.8% previously with a permanent loss of output of 10% of GDP relative to the pre-COVID-19 path (11).

(For more details on our Asia Pacific macroeconomic view, see "Asia-Pacific Quarterly: The Cost Of Uncertainty," published Dec. 2, 2019.)

Other emerging markets

The emerging markets story is generally less optimistic, particularly outside of East Asia, although with wide variations. Authorities are struggling with the balance between containing the spread of the virus and managing pressure to reopen economies. This is resulting in longer, more erratic, and more damaging lockdowns on average.

This is most prevalent in Latin America, where Brazil has become the new epicenter of the pandemic. We are marking down our 2020 GDP forecast in Latin America by 2 percentage points relative to our previous forecast solely due to the pandemic (our earlier economic assumptions remain valid). We now see output in Brazil falling 7% this year.

Europe, Middle East, and Africa (EMEA) economies remain close to our previous forecast with infection curves flattening and activity rising gradually. Turkey has the strongest recovery in this group with Russia having a relatively small output gap; South Africa is lagging. A stable-to-weaker US dollar should help keep inflation in check in emerging markets, along with lower oil prices and weak demand.

Central banks have lowered policy rates, aiming to stimulate activity while ensuring capital outflow pressures remain contained. Fiscal policy has been less forceful than in the advanced markets owing to less policy space.

(For more details on our emerging markets macro and credit view, see "Credit Conditions Emerging Markets: Slow Recovery, Prevalent Risks," published July 1, 2020.)

Contours of the Recovery And the Post-COVID-19 World

With the worst of the pandemic behind us in many countries, the focus has turned to the recovery. Given the nature of the COVID-19 shock — a self-imposed reduction in social mobility designed to contain the spread of a virus generating dramatic effects on economic activity and the unprecedented policy response —we will take a closer-than-normal look at the recovery scenario.

Constructing the recovery scenario involves determining the post-COVID-19 potential output path, as well as the transition from the current position to that path. These will take place against an economy with significantly stressed balance sheets that will need to be normalized.

Balance sheets and transition paths

The length of the COVID-19 shock is critical for assessing the role that balance sheets play in the recovery. This is important since balance-sheet recessions —such as the Global Financial Crisis — normally entail a larger loss of output (and perhaps potential growth) and a slower recovery relative to shorter, garden variety business cycle downturns.

A short shock with a V-shaped recovery would arguably inflict manageable damage to balance sheets as firms and households would have sufficient cushions to retain expenditures and there would be limited need for government spending and higher debt. The economy could be rebooted quickly as lockdowns end and social distancing restrictions are lifted.

However, the longer the lockdown, the higher the stress to the balance sheets and the real economy. For the affected households, a protracted lockdown means a significant reduction or loss of income. Expenses will be cut, particularly for discretionary purchases, and balance sheets will be tapped (assets will be drawn down) to preserve necessary consumption.

Precautionary savings may rise given uncertainties about how COVID-19 will play out in terms of both depth and duration. For example, US households are so far saving their government transfers (12).

Firms need to meet payroll, pay the rent, and pay creditors and suppliers. With revenue reduced in sectors such as hospitality and travel to due lockdowns, this means running down financial assets or finding new sources of financing by increased borrowing. Investment is likely to suffer in this environment, particularly where uncertainty around future demand is high and inventories are rising due to a concurrent demand shock.

For SMEs in particular, financing options may be limited and financial cushions less deep. So once financing sources are tapped out, closures may follow. Longer and deeper shocks to private demand and employment mean that the government will step in, as it has, expanding its balance sheet by issuing debt and enacting transfers to firms and households to cushion the blow and maintain businesses afloat.

Normalizing after COVID-19 thus implies adjustments across multiple sectors; desired balance sheets need to be restored. The longer and deeper the COVID-19 shock lasts, the more damage is done and the longer the adjustment process. Firms surviving COVID-19 will need to rebuild cushions or pay off debt accumulated in the crisis.

Households may need to rebuild assets if those were tapped and catch up on postponed purchases. Some workers will need to find new employment, perhaps in a different sector as firms may have closed and the composition of activity may have changed.

That requires time to learn new skills. Last but not least, governments will need to put their finances on a sustainable trajectory. This means higher taxes or lower spending and transfers, dampening demand further or elongating the recovery.

The length of the lockdown and the extent of balance sheet damage is where health policy success meets macro and financial economics. In our country forecasts, we sort these into three buckets. Those countries that are successful in flattening the curve are the "early exiters."

They will in general have less damage to balance sheets and a relatively smooth — but still difficult — transition to the vaccine discovery and dissemination stage, and ultimately to the new normal. Much of East Asia and Germany are in this group.

An intermediate group of "lagging exiters" will have a longer mitigation period with perhaps some elongated or mini second waves and a correspondingly more complicated transition period to the new normal. This group comprises some advanced economies, as well as higher-performing emerging markets.

The "late exiters," including a number of emerging markets struggling to contain the virus, will see an even longer mitigation period, more damage to the economy, and the most difficult transition.

The post-COVID-19 potential path

We now turn the potential path of the macroeconomy. When analyzing the impact of the COVID-19 shock, we prefer to work in output levels rather than growth rates (for example, chart 7 shows a stylized advanced economy's output in levels, with the year-end 2019 level indexed to 100).

It's important to work in levels because growth rates are likely to swing wildly and therefore risk giving a misleading picture. The spectacular rates of decline noted above are likely to be followed by rebounds that could feature growth rates well into the double digits in the second half of 2020.

While impressive on the surface, these won't fully reverse the steep drops in the first half of the year. Indeed, we expect the level of output in nearly all economies to remain below the year-end 2019 level for several years. Therefore, gauging progress in the recovery period is best done in levels, not rates.

The potential output path is defined as the economy operating at full resource capacity. That is, when all transitional effects have unwound. In the post-COVID-19 case, these effects include not only the discovery and dissemination of a vaccine, but also the market- and policy-driven return to normal activity and balance sheets.

It also includes any structural changes to the economy such as more resources for health security, more working from home, and more e-everything. A return to this path will take several years. This path need not be the same as the pre-COVID-19 path; indeed, we argue that it isn't.

The post-COVID-19 potential GDP path will be completely determined by the supply side of the economy since all transitional, demand-side effects are unwound. The supply side factors comprise the labor force, the capital stock, and total factor productivity (the efficiency at which labor and capital are combined) (see chart 7).

If none of the factors change as a result of the virus, then the pre- and post-COVID-19 paths are identical — this is the top line in the chart. Any change in the level of these three factors as a result of the virus will shift the level of the post-COVID-19 path relative to the pre-COVID-19 path — these are shown in the middle two lines in the chart.

The same logic applies for the rate of growth. Any change in the rate of growth of any of these factors will change the slope of the post-COVID-19 path relative to the pre-COVID-19 path — this is the bottom line in the chart.

Where do we come out? In our forecasts (see regional reports), we see early exiters as having potential GDP paths closer to the top line and the middle exiters being closer to the second line. The late exiters will look more like the bottom two lines, with larger output losses and the potential for slower post-COVID growth.

The speed of convergence to the post-COVID potential path will be determined by the intersection of social distancing constraints placed on activity and the amount of balance-sheet damage that needs to be restored (see chart 8).

Policy Settings Will Remain Accommodative Throughout The Recovery

The recovery path will also need to consider the evolution of policy, both fiscal and monetary. We expect the bulk of the focus to be on fiscal policy given its central role in demand creation, cushioning the worst effects of the COVID-19 shock and bridging to the recovery.

Public-sector deficits have skyrocketed as the result of the response to COVID-19. As the recovery builds, and output and employment rise, automatic stabilizers will kick in and deficits will narrow. The cyclically adjusted deficit will return to pre-COVID-19 levels as capacity utilization and the labor market recover. However, structural deficits will likely rise as governments ramp up health security spending.

Under our baseline scenario, financial markets remain relatively well-behaved. As a result, special facilities enacted by central banks to keep markets functioning — in the commercial paper and money markets, for example — should begin to unwind. This is analogous to what happened as the worst effects of the financial crisis ebbed.

Policy rates should remain at or near the lower bound for many countries over our forecast horizon. Asset purchase programs have ballooned central bank balance sheets. These will remain large, although asset purchase will taper during the recovery as managing monetary policy across two dimensions — the policy rate and medium-term yields via quantitative easing — is now firmly part of the playbook.

We expect some guidance on plans for reducing balance sheets as the recovery builds. Inflation pressures — particularly for (core) consumer prices — seem a distant threat at present.

Risks Remain Mostly On The Downside, With Significant Uncertainty

Health-related variables are the top risk to our forecast in the next 12 months. While we forecast a largely smooth baseline recovery path, this is predicated on an orderly withdrawal of social distancing restrictions and the appropriate human responses.

Should either the virulence of the virus or human behavior along the recovery path lead to a renewed rise in the infection rate, a reversal of social distancing restrictions and the negative impact on the recovery is likely. We are also adopting the current consensus medical views that a vaccine will become available by mid-2021. If the discovery or rollout of the vaccine takes longer, then the recovery will be correspondingly delayed.

The unintended consequences of quantitative easing on productivity in the nonfinancial corporate sector are also a risk. There are two channels. One is asset prices, which are likely to rise as a result of quantitative easing, thereby lowering debt-to-equity ratios, all else constant (13). A second channel is interest rates across the maturity spectrum.

These are likely to fall owing to quantitative easing, which would raise earnings-to-interest coverage ratios. Both of these channels risk prolonging the lifespan of weaker firms that would otherwise exit the market. The effect would be to pull down productivity and growth.

Policy errors along the uncertain recovery path are another concern. On the fiscal front, premature austerity in reaction to elevated government debt levels could result in public-sector demand being withdrawn before private-sector demand fully recovered. This would blunt the recovery, as happened following the Global Financial Crisis.

On the monetary front, the measurement of output gaps, and inflation and employment pressures will be complicated by the fact that the authorities will not know in real time whether the economy is on a slow, medium, or fast path using the typology above.

Given the current uncharted waters, this risk is larger than for a typical cyclical downturn. This can lead to overestimating inflation pressures and setting monetary policy rates that are too restrictive, hurting output and employment and undershooting the inflation target, or vice versa.

Finally, expectations around the normalization of government and central bank balance sheets will need to be addressed as the COVID-19 crisis wanes. Each of these entities across a number of geographies has seen an explosion of balance sheet sizes. (These are related: a fair chunk of the rise in central bank assets is the rise in government bond holdings.)

The risk is that interest-rate expectations or inflation expectations become unanchored in the absence of a credible path to normalize these balance sheets. While the path of short-term interest rates and inflation is lower at present owing to a large negative demand shock, this is not guaranteed in a post-COVID-19 world. — S&P Global Ratings

These were the details of the news The global economy begins a slow mend as COVID-19 eases unevenly for this day. We hope that we have succeeded by giving you the full details and information. To follow all our news, you can subscribe to the alerts system or to one of our different systems to provide you with all that is new.

It is also worth noting that the original news has been published and is available at Saudi Gazette and the editorial team at AlKhaleej Today has confirmed it and it has been modified, and it may have been completely transferred or quoted from it and you can read and follow this news from its main source.

{kind=link}