{kind=link}

BERLIN, GERMANY – JUNE 27: General view of the Peloton stores in Berlin on June 27, 2020 in Berlin, … [+] Germany. (Photo by Jeremy Moeller / Getty Images)

Getty Images

Peloton (NASDAQ: PTON) is a home fitness company that sells connected exercise bikes and treadmills and related fitness subscriptions. Inventory has grown more than four times since the start of the year as the Covid-19 pandemic and associated lockdowns resulted in people stopping to go to gyms and fitness centers and exercising from home, leading to increased demand for products and Company services led. Peloton is now trading at 8 times projected sales for FY21, ahead of Apple at 6.5 times sales. Does it make sense? We think it is. In this analysis, we take a look at the company’s finances, future prospects and valuations. Check out our interactive analysis Peloton Rating: Expensive Or Cheap? for more derailments. Parts of the analysis are summarized below.

An overview of Peloton’s business

Peloton Interactive sells connected fitness equipment such as bicycles (starting at approximately $ 1,900) and treadmills (starting at approximately $ 2500) with monthly Connected Fitness subscriptions ($ 39 per month) that provide boutique instructor-led classes to user bikes and the Peloton Digital Broadcast and sync membership ($ 13 per month), which broadcasts classes to mobile devices and smart TVs. The company’s product and service package is an alternative not only to other training equipment, but also to fitness studios and memberships in fitness centers. Although the prices for the company’s products are very high, the ecosystem that combines hardware, software, and content is quite affordable when compared to fitness classes and subscriptions. For perspective, the average monthly gym membership cost in the US in 2018 was about $ 58. [1] While Peloton sells primarily to private individuals, it is also involved in the retail and hospitality sectors.

Pelotons finances

Peloton has grown rapidly. Revenue rose from approximately $ 440 million in fiscal 18 (fiscal year ended June) to approximately $ 1.83 billion in fiscal 20 – an annual rate of over 100%. Equipment sales rose from approximately $ 350 million in Fiscal 18 to $ 1.46 billion in Fiscal 20, with the company shipping 626,000 bikes and treads in 2020 alone. Subscription revenue increased from approximately $ 80 million to $ 360 million as the company’s number of affiliated fitness subscribers rose from 246,000 in fiscal 18 to approximately 1.09 million in fiscal 20. The total number of Peloton members increased to 3.1 million by the end of fiscal 20, including users who only pay for the digital subscription (not connected to the equipment). In FY21, we expect Peloton revenue to grow to nearly $ 3.6 billion, driven by continued growth in device sales and a growing customer base.

While Peloton continued to lose money over the past year, the viability of its business looks favorable. Overall, gross margins in fiscal year 20 are high at around 47%, while hardware margins are 43%. By comparison, even Apple – a symbol of hardware profitability – posted a gross margin of less than 40% over the last fiscal year. While Peloton’s operating costs tended to be higher, they grew more slowly than revenue. With sales expected to double this year, Peloton appears to be on track to become profitable.

Pelotons rating

Peloton stock is currently trading at a level of nearly $ 130 per share, which is roughly 8 times its forecasted revenue for FY21. While the rating multiplier may seem rich, we think it’s largely justified considering that Apple – the most established hardware / software / service game – is trading at around 6.5x. Peloton’s growth has been solid: sales have doubled each year for the past two years, and sales are expected to double in FY21 as well. Margins can also be improved significantly given the high gross margins and low customer acquisition costs. In addition, the company’s lucrative networked fitness subscription revenue is likely to be very low as users who have invested in expensive hardware are less likely to stop paying for monthly service. Also, given the craze for the company’s brand, there may be an opportunity to double up on lifestyle and apparel products against, for example, Lululemon and Nike

FROM

.

That said, there are also risks. First, Peloton is currently facing significant supply shortages. While a new manufacturing facility in Taiwan is slated to begin production by the end of the year, the company will likely still be missing out on potential vacation demand. Second, at the end of the Covid-19 pandemic, investors could rethink the valuation of “at-home” stocks and this could at least temporarily affect Peloton’s valuation. Regardless, tech giants – with their deep pockets and software ecosystems – could play a bigger role in connected fitness and challenge the peloton. For example, Apple recently launched its home workout app Fitness Plus, which offers guided workouts and connects to Apple devices like the Apple Watc

Trefis

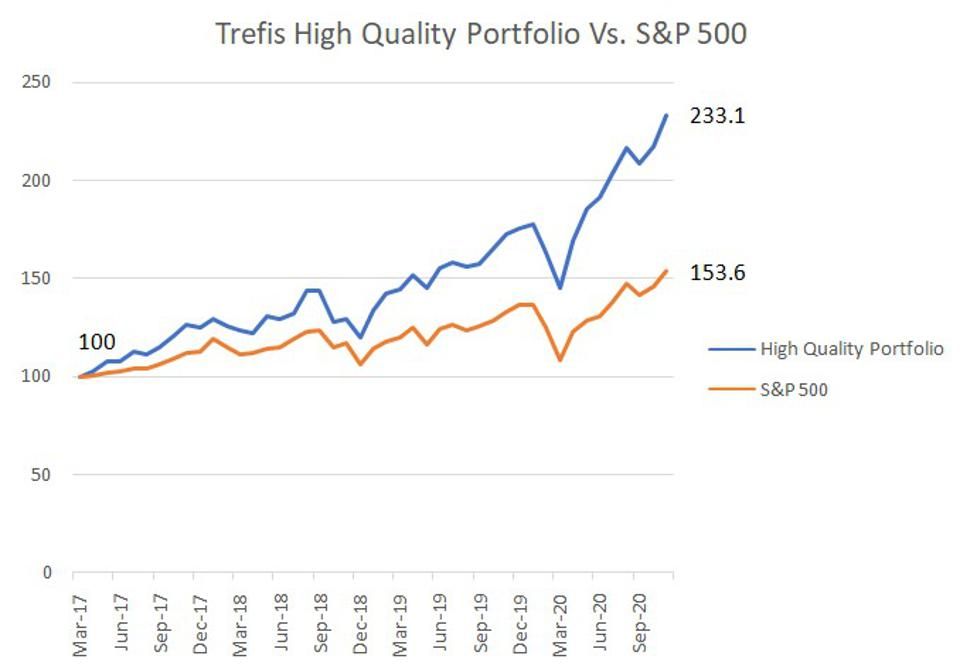

What if you want a more balanced portfolio instead? Here is a Quality portfolio to beat the marketWith a return of over 100% since 2016 versus around 55% for the S&P 500. Consisting of companies with strong sales growth, healthy profits, lots of cash and low risk, it has consistently outperformed the broader market year after year.

See everything Trefis price estimates and Download Trefis-Daten Here

What’s behind Trefis? See how it enables new collaboration and what-if CFOs and finance teams | Product, R&D, and marketing teams

These were the details of the news Why Peloton deserves a richer rating than Apple for this day. We hope that we have succeeded by giving you the full details and information. To follow all our news, you can subscribe to the alerts system or to one of our different systems to provide you with all that is new.

It is also worth noting that the original news has been published and is available at de24.news and the editorial team at AlKhaleej Today has confirmed it and it has been modified, and it may have been completely transferred or quoted from it and you can read and follow this news from its main source.