We show you our most important and recent visitors news details The US election, COVID-19 & commodities in the following article

Hind Al Soulia - Riyadh - By Ole Hansen

DUBAI — As we head into the final quarter of a year that many may wish never happened, the global pandemic will continue assert a major influence on the performance of different sectors: from energy and metals to agriculture. With the pandemic still developing and a vaccine probably months away, the only thing that remains certain is the uncertainty.

It will continue to create volatile and unpredictable market conditions, while geopolitical risks add another layer – not least considering what lies ahead, with the US Presidential election on Nov. 3 probably much closer than what the polls can measure.

Never in history have global interest rates been pushed so hard towards zero across so many countries simultaneously, with massive increases in fiscal deficits on top of historically high debt levels in the global economy.

Add to this government attempts to support growth through the spending of money that needs to be printed first, and the outlook for precious and some industrial metals continues to look supportive into Q4 and beyond.

The combination of central banks actively supporting the return of inflation and the potential for the dollar to weaken further remains key to our general bullish outlook for commodities, especially those that historically have helped preserve wealth during times of raised uncertainty and inflation.

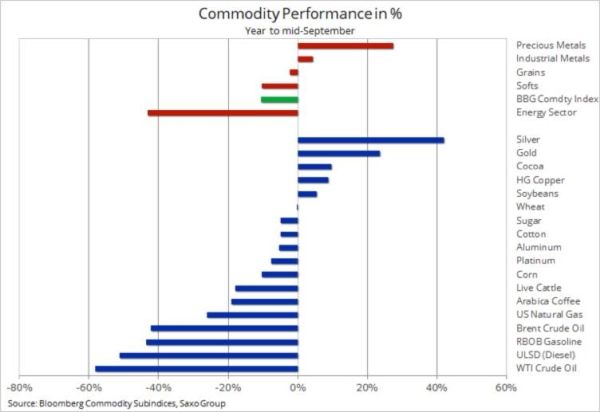

The year to mid-September performance among some key commodities tells a story about strong demand for precious metals amid the global collapse in rates and the rising risk that inflation will emerge to render government bonds already trading near zero or below useless as a means of safe haven.

China got the virus first and have subsequently managed a strong, debt-fueled recovery similar to the one seen following the 2008 Global Financial Crisis. The combination of COVID-related supply disruption, financial speculators looking for an inflation hedge and not least very strong demand from China driving down global stocks, have supported a strong year for industrial metals led by copper.

Eventually, we see the steep uptrend in HG Copper from the April low being broken, leading to a period of consolidation which we believe may occur in Q4. On that basis we see the short-term upside for copper as limited, with the potential driver for an extension being a renewed promise of infrastructure spending from the next US President — similar to the one Trump promised, but failed to deliver on, four years ago.

Following a year where gold is up more than 20% and silver double that, it is a bold call to look for further gains, at least in the short term. However, the powerful combination of rock bottom rates, rising demand for inflation hedges and the potential for a weaker dollar all point to further gains.

Following a prolonged period of consolidation around and mostly above $1,920/oz, we see gold eventually moving higher to finish the year at or near $2,000/oz.

Considering we have entered unchartered territory, it is difficult to provide a price estimate for 2021. However, using the decade-old price channel, the target for 2021 could be somewhere between $2,400 and $2,500/oz, some 20% above the mid-September trading area.

Silver has struggled to outperform gold after the ratio between the two metals returned to its ten-year average close to 70 ounces of silver to one ounce of gold. Given our positive outlook for gold, we see silver continuing higher, perhaps with a slight underperformance given our neutral view on industrial metals.

Platinum’s record discount to gold may eventually attract some renewed investor interest, not least considering the outlook for the market moving into a deficit this year. A break below two in the gold-platinum ratio could potentially signal a move to 1.8, a 10% outperformance.

The crude oil market is likely to remain stuck, with Brent crude spending most of the final quarter trading in the 40s before eventually moving higher into the 50s during the first half of 2021. On that basis, we raise our Q3 range by three dollars to a $38-$48 corridor.

The battle between OPEC+ production cuts and an uncertain demand outlook escalated in September, with Saudi Arabia showing their growing frustration about crude oil’s inability to rally further.

It led to strong verbal intervention by the Saudi Energy Minister, who blamed cheaters and short sellers for the lack of progress. While cheating is a clear problem that needs to be addressed and short sellers may move the market for a short period of time, fundamentals which are currently weak amid an abundance of fuel and low demand will always be the main driver.

We remain cautious about crude oil’s short-term ability to rally much further, unless OPEC+ surprises the market by abandoning its planned 2 million barrels/day production increase set for January. While the UAE, a major recent laggard, will cut production again, some concerns linger with regards to Iraq, a notorious cheater, and Libya, which will try to increase production following its ceasefire announcement.

— The writer is head of commodity strategy at Saxo Bank

These were the details of the news The US election, COVID-19 & commodities for this day. We hope that we have succeeded by giving you the full details and information. To follow all our news, you can subscribe to the alerts system or to one of our different systems to provide you with all that is new.

It is also worth noting that the original news has been published and is available at Saudi Gazette and the editorial team at AlKhaleej Today has confirmed it and it has been modified, and it may have been completely transferred or quoted from it and you can read and follow this news from its main source.

{kind=link}