We show you our most important and recent visitors news details Gold consolidates strong gains; downside risks mount for crude in the following article

Hind Al Soulia - Riyadh - By Ole Hansen

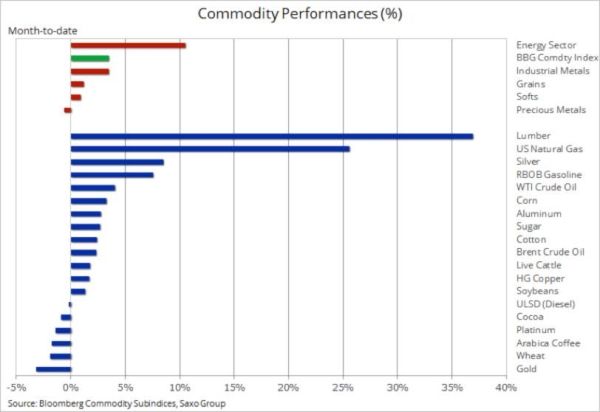

DUBAI — The commodity sector has maintained positive momentum so far this August with the Bloomberg Commodity Index trading higher for a fourth consecutive month. However, following the pandemic-led collapse during the first quarter, the year-to-date performance remains in the red by 11%. Gains have so far this month been broad-based, led by the energy sector and industrial metals.

The risk of rising inflation and the weaker dollar remain two key supporting themes that continue to attract attention. Improved U.S. data earlier in the month and the lukewarm approach to yield-curve control that was signaled in the latest FOMC minutes have led to a small rise in bond yields this month. This has helped to trigger profit-taking in gold which, following its July 8.5% rally, has run into consolidation. This helps to explain why it is found at the bottom of the table while silver, in third place, has managed to build on its 30% rally last month.

Lumber, a small futures market that we do not normally spend time on in this update, has climbed to the top of the leaderboard, hence it’s deserving of a closer look. Home improvement companies around the world have experienced strong demand from stay-at-home consumers spending money on their home instead of going out. In the US this trend can be seen through the strong performance and recent comments from Home Depot (HD) and Lowe’s (LOW). Both stocks have more than doubled since the March low as customers have flocked to their stores to buy goods, including lumber.

The Random Length Lumber Futures for September delivery have rallied by 98% year-to-date to reach a record $801/1000 board feet, more than double the average price during the past ten years. Apart from increased demand from stay-at-home consumers, record low interest rates have spurred a jump in new constructions. This, at a time where inventories are low due to tariffs US President Trump introduced on lumber imports from Canada. The price has moved deep into overbought territory following several consecutive days of finishing at the daily limit allowed by the exchange.

HG Copper reached a fresh two-year high this past week, thereby continuing its strong recovery from the pandemic lows in March. Apart from the recent dollar weakness, demand, especially in China and more recently in the US, it has recovered strongly. Adding to this is a pandemic-related reduction in supplies of mined copper and scrap. These developments have led to sharp declines in stockpiles at exchange-monitored warehouses, not least on the London Metal Exchange (LME) where stocks have fallen rapidly to a 13-year low, thereby raising short-term supply concerns.

But copper’s continued advance depends to a certain extent on how much of the rapid inventory drop has been driven by speculation and how much is actual demand. Increased focus for inflation hedges, which have triggered strong demand for gold and inflation-protected bonds in recent months, may also have impacted the demand for other hard assets, such as copper. We remain skeptical about copper's ability to move higher at this stage where an economic dark cloud continues to hang over the market. A weekly close above $3/lb in New York and $6,600/t in London will be needed before any talks about a potential 10% extension to $3.3/lb.

Crude oil has traded sideways since June and during this time both WTI and Brent crude oil have struggled to respond in either direction to economic data and specific oil market news. The stability seen at a time where the OPEC+ group of producers have turned on their taps has been taken as good news by some, while others worry about crude oil’s inability to move higher in response to the recent dollar weakness and continued stock market strength.

The range-bound oil market has also seen the recovery in large-cap US energy stocks stall with the S&P 500 Index ETF (SPY:arcx) having outperformed the Energy Select Sector SPDR ETF (XLE:arcx) by more than 15% since early June, when the impressive rally in WTI and Brent crude oil from the April low began to stall after both returned to a 40-dollar handle.

The short-term outlook remains challenging with a continued price recovery being tempered by downbeat comments on the economic outlook from the US Federal Reserve and OPEC+. Following their latest Joint Ministerial Monitoring Committee (JMMC) meeting on Thursday, the group said they saw demand recover slower than expected. A stronger and more prolonged second wave of infections could further reduce its overall demand forecasts in the coming months. With this mind, the group is likely to step up its efforts to reign in up towards 2.3 million barrels/day (Reuters) of production from countries currently producing above the agreed targets.

Not least after Libya’s government announced a cease-fire Friday. The prospect of Libya, currently producing less than 100,000 barrels/day, now being able to increase production would add further delays to the rebalancing process and it helped to explain the weakness seen in oil prices ahead of the weekend. Brent remains stuck in a narrowing three-dollar range between its 50-day and 200-day moving averages at $43.30 and the 200-day at $46.25.

Gold and silver, two of the best-performing assets in 2020, have both run into an overdue correction following a three-week surge that took gold to a new record high above $2000/oz and saw silver reach $30/oz after almost touching $12/oz during the dash-for-cash panic sell-off in March. Both metals are now set to be engulfed in a battle between short-term technical traders looking to sell, and longer-term buyers who worry about the economic outlook while seeking protection against the risk of an oncoming period of inflation.

So far the market has been hit by two bouts of profit taking. The first one following the recovery in US real yields in response to improved US economic data and the second, this past week when minutes from the latest FOMC meeting revealed a certain hesitancy of moving towards an implementation of yield-curve control.

Overall, we maintain a bullish outlook for gold and silver with loose monetary and fiscal policies around the world supporting not only gold and silver, but potentially also other mined commodities. Real rates — as highlighted earlier — remain by far the biggest driver for gold and the potential introduction of yield-curve control combined with the risk of rising inflation — as the US authorities look to overstimulate the economy — should see those rates remain at record low levels, thereby supporting demand for metals.

An increasingly fraught US elections season combined with current US–China tensions are likely to add another layer of support through safe-haven demand. The potential for even lower real rates should also support a continued weakness of the dollar, thereby creating the trifecta of drivers that should support investments in precious metals.

However, what the market needs in the short term is to consolidate its strong gains. On that basis we see the potential upside above $2000 limited until the market gets used to and feels comfortable with the current levels. Given how far the market has travelled already this year, a correction could be relatively deep. Using Fibonacci we focus on support at $1920 which also is the previous record high from 2011, followed by $1873 and $1825.

— The writer is head of commodity strategy, Saxo Bank

These were the details of the news Gold consolidates strong gains; downside risks mount for crude for this day. We hope that we have succeeded by giving you the full details and information. To follow all our news, you can subscribe to the alerts system or to one of our different systems to provide you with all that is new.

It is also worth noting that the original news has been published and is available at Saudi Gazette and the editorial team at AlKhaleej Today has confirmed it and it has been modified, and it may have been completely transferred or quoted from it and you can read and follow this news from its main source.

{kind=link}